Money Advisor - What's Important to Know/Consider Before Trusting Anyone With Your Finance

Money Advisor - What's Important to Know/Consider Before Trusting Anyone With Your Finance

Here’s the deal: There are many people in finance that appear to be helping you, yet in reality, they are selling you something. A product, a plan, a subscription — whatever it is, their income depends on you buying it. That's not inherently wrong, but it does mean you need to know what you're actually getting before you hand over your trust and your money.

Finding a genuine money advisor — someone who gives you a gameplan that fits your actual life, not a cookie-cutter recommendation designed to move product — makes a real difference. I've seen it change people's financial trajectories completely. And I've also seen people get burned by advice that sounded polished but wasn't built for them.

So here's what I actually look at when evaluating whether a financial advisor is worth working with.

They Should Know Your Numbers Before They Know Their Recommendations

A good money advisor doesn't walk in with a product already in mind. They start by understanding where you are. What do you earn? What do you owe? What does your monthly cash flow actually look like? What are you trying to build?

If someone starts talking to you about investment accounts before asking about your debt situation, that's a flag. You can't build up while you're hemorrhaging money on interest every month. A real advisor sequences things correctly: cash flow first, debt strategy second, protection third, then growth.

If they're skipping steps to get to the thing they make money on, that's not a money advisor — that's a salesperson with a license.

A Good Debt Advisor Helps You See Debt Differently

One of the most useful things a great advisor can do is reframe how you think about debt. Not all debt is the same. High-interest consumer debt is a drain. A home equity line used strategically is a tool. Business credit used for cash-flowing assets is different from a credit card used for lunch.

A debt advisor worth their salt will help you understand the difference and build a paydown strategy that actually fits your cash flow — not just a priority list based on interest rates alone.

Velocity banking is one example of this. Instead of making minimum payments and throwing extra at the principal when you can, you run your income through a line of credit to reduce your average daily balance. That's how people pay off mortgages in 5 to 7 years on the same income they were making before. It's not magic — it's math, applied intentionally.

The right advisor can show you the math for your specific situation. That's what a session at denzelrodriguez.com/services-page is built around.

Watch Out for These Red Flags

I've talked to a lot of people who came to me after working with advisors who weren't a good fit. Here are the patterns I hear most often:

They got a plan built around products the advisor was affiliated with. Life insurance used as an investment vehicle from someone who gets a commission on it. An annuity recommended to someone in their 30s. A mutual fund with a 5% load fee.

They were told to "just invest in the market" while carrying 22% APR credit card debt. That math doesn't work. Market returns don't consistently beat high-interest debt.

They paid a retainer for advice they never implemented because nobody helped them with the accountability piece. A plan you don't follow isn't a plan — it's a document.

The best advisors aren't just smart about money. They help you follow through.

What to Expect From a Real Financial Consultation

When I sit down with someone, the goal isn't to impress them with strategies. The goal is to walk away with a clear, specific plan they can start acting on that week.

That usually means identifying the two or three moves that will have the biggest impact right now — not in five years, right now. It might be restructuring how income flows through accounts. It might be disputing an inaccurate item on a credit report. It might be stopping an automatic transfer that's been quietly draining a savings account.

The specifics depend on the person. That's the point.

Real financial guidance is personal. It takes your numbers, your goals, your family situation, and your actual cash flow into account. If you've gotten advice that felt generic, it probably was.

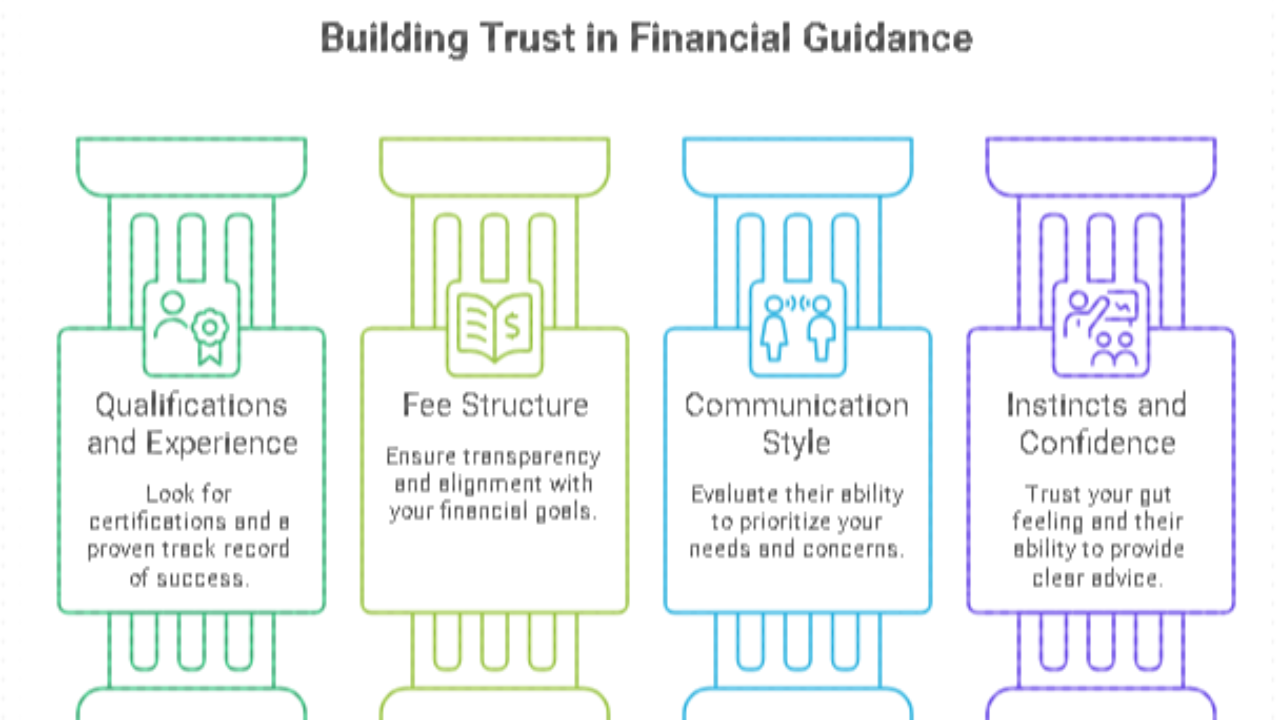

How to Find Someone Worth Working With

Ask these questions before you commit to anyone:

How do you get paid — fee-only, commission, or a mix? What's your background with debt payoff strategies specifically? Can I talk to someone you've worked with before? What does the follow-up process look like after our first session?

Their answers will tell you a lot. Someone who gets defensive or vague about compensation probably has a conflict of interest they'd rather you not think about.

If you want to talk through your situation with someone who's going to be direct with you, reach out here and we'll figure out together whether working together makes sense.