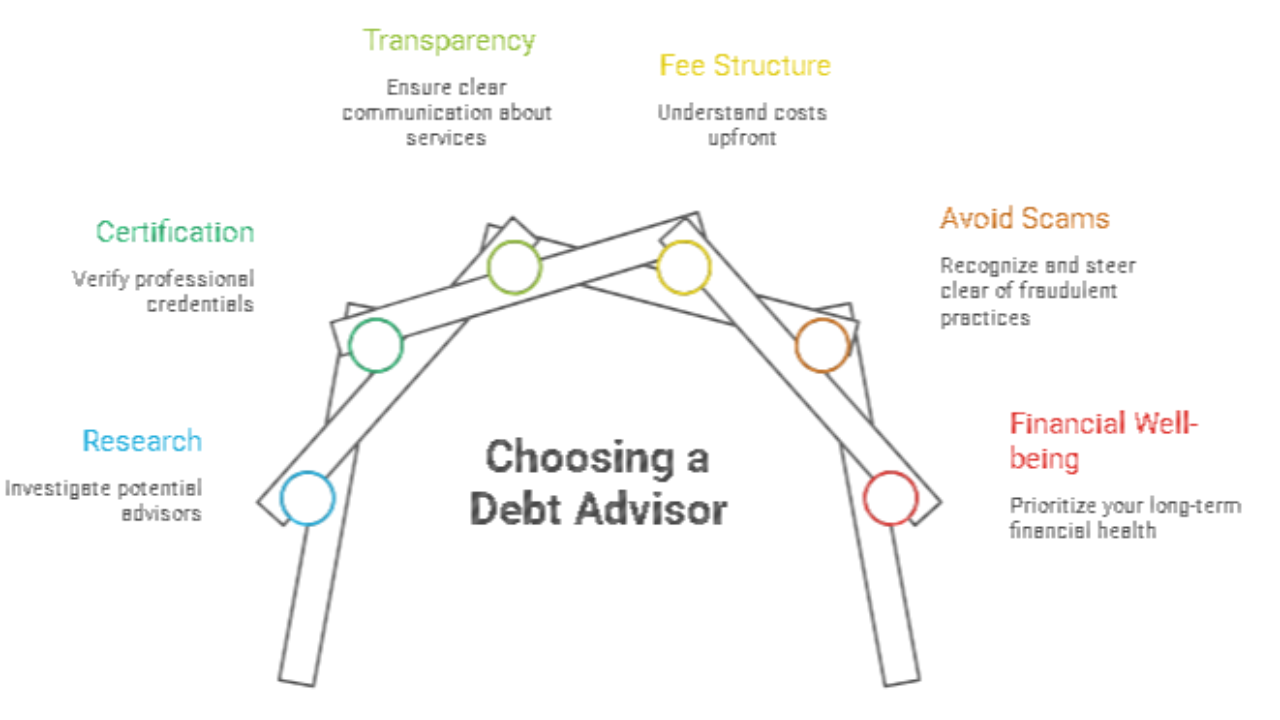

Debt Advisor: How to Get Real Help Without Getting Taken Advantage of

Debt has a way of making people desperate. And desperate people make easy targets.

That's the honest truth about why the "debt relief" industry has so many bad actors in it. When you're stressed about what you owe, when the calls are coming in and the balances don't seem to move, you'll sometimes pay someone to make it stop — even if their solution creates new problems.

A genuine debt advisor doesn't work like that. Their job is to put you in a better position than you're in right now, not to collect a fee while your credit gets torched. But knowing the difference between real help and a trap? That's what I want to walk through here.

What a Debt Advisor Actually Does

At its core, a debt advisor does two things: they analyze your situation clearly, and they help you build a plan you can actually follow.

That means looking at every debt you carry — the balance, the interest rate, whether it's in collections, whether it's personal or business — and building a payoff sequence that fits your real cash flow. Not a generic list. Your list.

Good money management starts with understanding where the money is going. A lot of people are surprised when they sit down and map it out for the first time. They didn't realize how much they were paying in interest each month. They didn't realize that one account had been quietly accumulating fees. They didn't realize that a different paydown order would free up cash faster.

That kind of clarity is what changes behavior. Not willpower. Clarity.

The Difference Between Debt Advising and Debt Settlement

This distinction matters, so I'm going to be clear about it.

Debt settlement is a specific service where a company negotiates with your creditors to accept less than what you owe. During that process, you typically stop making payments — which tanks your credit score. The settlement company collects fees. Your accounts go delinquent. And the forgiven amount may be treated as taxable income by the IRS.

That's not always the wrong choice. In genuine hardship, it might be the only path. But it's often sold to people who had better options they didn't know about.

A debt advisor helps you understand all the options before you commit to any one of them. Credit assistance — disputing inaccurate items, negotiating directly, restructuring payment plans — can often accomplish similar goals without the credit damage.

If someone leads with settlement before understanding your full picture, that's a sign they're selling a product, not solving a problem.

How Velocity Banking Changes the Math

One of the strategies I use most with clients carrying significant debt is velocity banking. Here's the core of it.

Most people have a checking account that money flows in and out of, and they make regular payments on their debts. Their money sits in checking earning nothing, and they pay interest on loans daily.

Velocity banking replaces that passive approach. You use a home equity line of credit or business line of credit as your primary account — your income goes in, your expenses come out. Because a line of credit calculates interest on the average daily balance, every dollar you earn works against your debt the moment it lands.

Done consistently, people pay off mortgages in a fraction of the original timeline without increasing their income. The math is real. I've walked clients through it who thought they were 25 years from payoff and ended up debt-free in 6 or 7.

The strategy doesn't work for everyone — you need a line of credit and more income than expenses. But if you qualify, it's worth understanding in detail.

Credit Assistance: What It Is and What It Isn't

A big part of debt advising involves the credit side. When debts go unpaid or get sent to collections, your credit score reflects it. And that score affects your ability to get housing, business financing, and anything else that requires a credit check.

Real credit assistance means helping you understand what's on your report, whether any of it is inaccurate (more common than people think), and what can be disputed or addressed directly with creditors. It means building positive history through responsible use of new accounts while the negative items age off.

It does not mean paying a company $99 a month to "remove negative items" from your credit report through some proprietary process. That's not how credit repair works. Legitimate negative items don't disappear because someone sends a dispute letter on your behalf — they come back.

Sustainable credit improvement takes time. Anyone promising fast results should be asked a lot of follow-up questions.

If you want to look at your actual credit picture alongside someone who can help you build a real plan around it, the services at denzelrodriguez.com is the place to start. The 1-on-1 consultation is built specifically to give you a gameplan you can act on the same week.

What to Bring Into a Debt Advising Session

If you're ready to sit down and work through this, come prepared with:

Your current balances on every account — credit cards, loans, mortgage, business debt. Your monthly take-home income. A rough sense of your monthly expenses. Your most recent credit report (you can pull this free at AnnualCreditReport.com).

You don't need to have everything figured out. That's what the session is for. But the more specific your numbers, the more specific the plan can be.

Connect here when you're ready to have an honest conversation about where you are and what it's actually going to take to get where you want to go.

FAQ

What is a debt advisor?

A debt advisor helps you understand your debt situation — balances, interest rates, payoff options — and builds a repayment strategy that fits your actual cash flow. Good debt advisors also cover credit improvement and money management as part of a complete financial picture.

Is debt advising the same as debt consolidation?

No. Debt consolidation is a specific product — you take out one loan to pay off multiple debts, ideally at a lower rate. A debt advisor helps you evaluate whether that's a good option for you, along with other strategies like velocity banking, direct negotiation, or accelerated payoff. Advising is the analysis; consolidation is one possible outcome.

Can a debt advisor help with business debt?

Yes. Business debt has its own structure — lines of credit, equipment financing, accounts payable — and a good advisor will look at personal and business debt together to see how they interact. Sometimes business cash flow can be used to accelerate personal debt payoff, and vice versa.